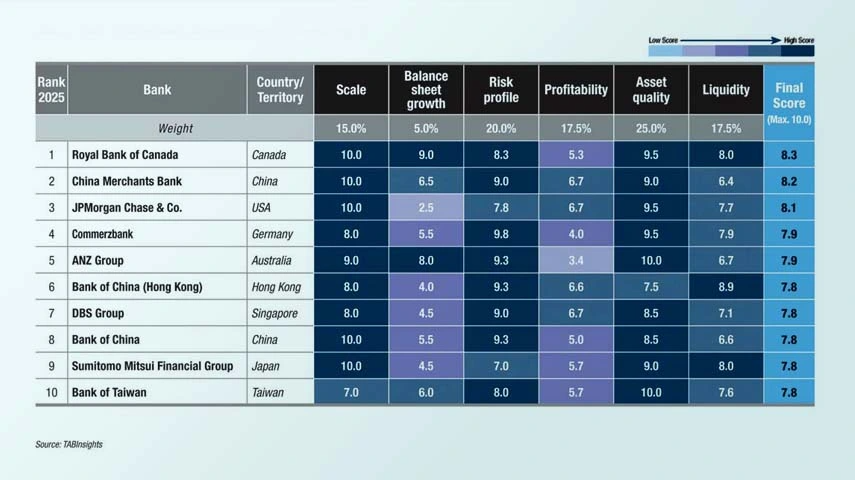

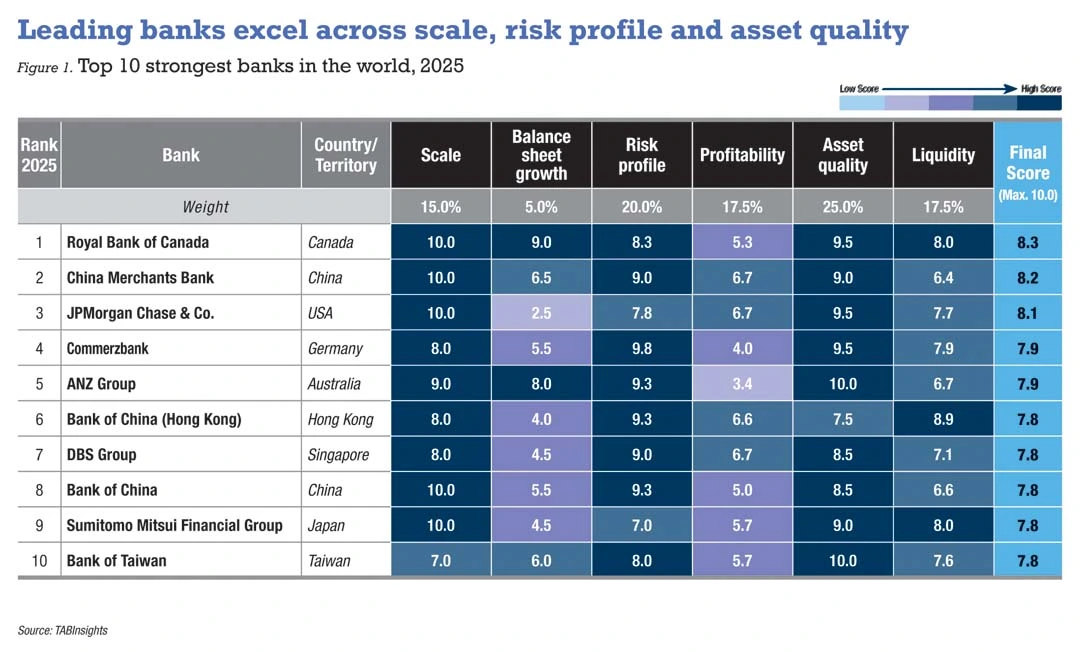

Royal Bank of Canada, China Merchants Bank and JPMorgan Chase hold the top three positions in the TAB Global 1000 World’s Strongest Banks ranking for 2025. The ranking covers 1,000 banks from 100 countries, territories and special administrative regions, evaluating their performance in the financial year (FY) 2024, with a cutoff date at the end of March 2025.

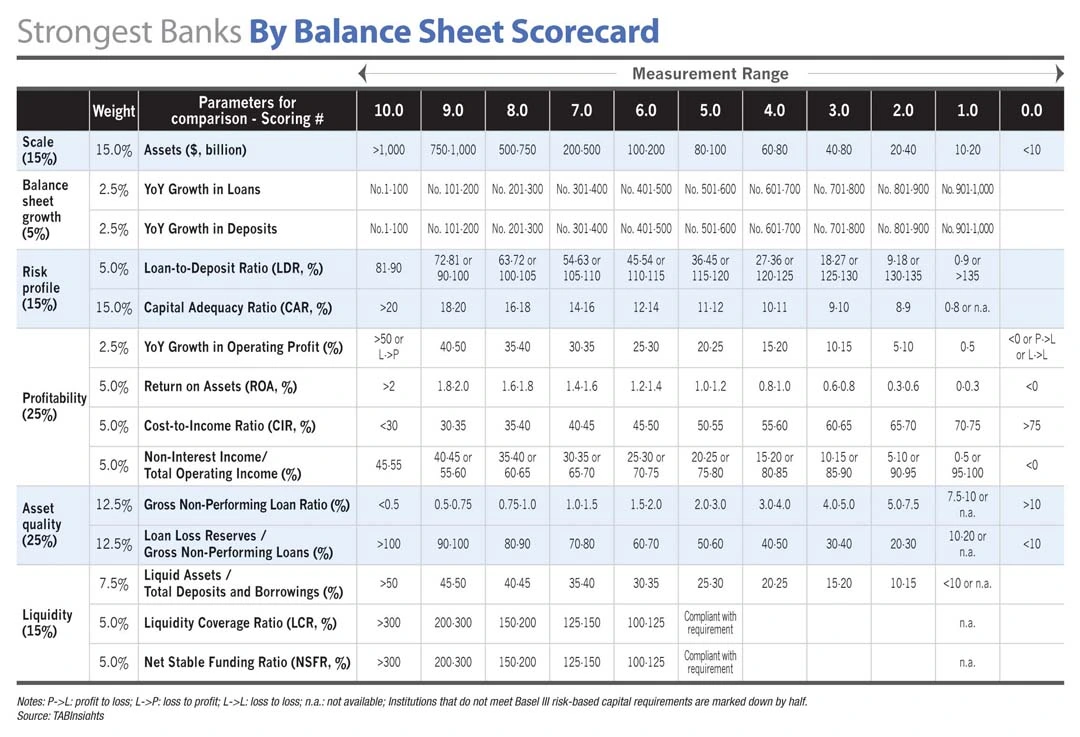

The TAB Global 1000 World’s Strongest Banks ranking evaluates the 1,000 largest banks worldwide based on balance sheet strength. It employs a detailed and transparent scorecard to assess banks and financial holding companies across six criteria: scale, balance sheet growth, risk profile, profitability, asset quality and liquidity, comprising 14 specific factors.

The ranking includes 432 banks from Asia Pacific, 223 from Europe, 155 from North America, 84 from Latin America and the Caribbean, 64 from the Middle East, 34 from Africa and eight from Central Asia, with some adjustments to regional classification compared with last year. Notably, the strongest banks in markets including Australia, Canada, China, Germany, Hong Kong, Hungary, Israel, Japan, Mexico, Saudi Arabia, Singapore, Taiwan and the United States (US) are all in the top 20.

The global banking sector remained broadly stable in FY2024. Regional differences continued to shape performance, with emerging markets benefiting from higher lending spreads and stronger loan demand but facing elevated credit and liquidity pressures, while advanced markets maintained stable asset quality and diversified income, albeit with persistent constraints on profitability and efficiency.

Return on assets (ROA) held steady, although margins were compressed due to competitive pressures and higher funding costs. Operational efficiency improved modestly despite rising technology and regulatory expenses, with Central Asia and the Middle East reporting the lowest cost-to-income ratio (CIR), while North America and Europe continued to face higher structural costs. Income diversification progressed gradually, with banks in North America and Europe contributing a higher share of non-interest income to total operating income, whereas Asia Pacific, the Middle East and Central Asia remained largely reliant on lending.

Asset quality remained broadly resilient, although Africa, Latin America and the Caribbean, and Central Asia showed higher credit vulnerabilities. Elevated loan-to-deposit ratios in Central Asia and Latin America and the Caribbean suggest relatively stretched positions, while Asia Pacific, the Middle East and Europe operated within more balanced ranges. Liquidity largely remained sound, and capitalisation improved slightly, with European, Central Asian and Middle Eastern banks maintaining stronger positions.

Earnings strength and resilience underpin top 10 banks

Royal Bank of Canada ranks first globally with a score of 8.3 out of 10, supported by a diversified model across business segments and geographies, prudent risk management and solid capital and liquidity position. Within the top 10 strongest banks, Royal Bank of Canada derived 51.3% of its operating income from non-interest sources in FY2024, the highest among its peers. Its asset quality remained strong, with a gross non-performing loan (NPL) ratio of 0.6% in FY2024, while liquidity was robust, reflected in a liquid assets-to-total deposits ratio of 52% and a liquidity coverage ratio (LCR) of 128%.

The acquisition of HSBC Canada, completed in March 2024 as the largest deal in Royal Bank of Canada’s history, expanded its client base and global banking capabilities and created opportunities for cost synergies and growth. Beyond Canada, the bank continues to build scale in the US and expand in Europe and other regions, supporting long-term diversification.

China Merchants Bank holds the second position globally, underpinned by a stronger risk profile and higher profitability than Royal Bank of Canada. Its ROA declined slightly to 1.3% in FY2024, while its CIR improved to 34.1%. The bank has been steadily reshaping its business mix, with non-interest income rising to 37.3% of operating income, signalling greater diversification beyond lending. At the same time, its capital position strengthened, with the total capital adequacy ratio (CAR) rising to 19.1% from 17.9% in FY2023.

Although China Merchants Bank’s liquidity remains weaker than Royal Bank of Canada, it has improved in recent years. A strong retail franchise and access to affluent clients underpin its stable deposit base and funding cost advantage. Its deposit growth has consistently outpaced loan growth, reducing the net loan-to-deposit (LDR) from 88% in FY2019 to 72% in FY2024, while reliance on short-term wholesale funding has declined.

JPMorgan Chase occupies the third spot globally, backed by a broad range of services, strategic technology investments and a “fortress balance sheet” philosophy emphasising strong liquidity, low leverage and robust capital. The bank has expanded its market share across multiple business lines while maintaining strict risk discipline. Its profitability strengthened, with ROA rising from 1.3% in FY2023 to 1.4% in FY2024, CIR falling from 53.7% to 52.7% and non-interest income as a share of total operating income increasing from 42.4% to 45.4%. The bank also maintained strong asset quality and solid capitalisation, with a CAR of 17.9%, alongside robust liquidity reflected in a liquid assets-to-total deposits ratio of 64%.

Commerzbank, now the strongest bank in Europe, rose to fourth globally, benefit from sharper profitability and an improved risk profile. Its ROA, CIR and non-interest income ratios all improved, with CIR falling to 58.5% in FY2024 due to robust income growth across multiple business lines, aided by restructuring and digital investments. Stronger capitalisation — Tier 1 capital ratio rising to 17.6% and total CAR to 20.9% — reinforced resilience, while its risk profile was the highest among the global top 10. Asset quality also held firm, with its gross NPL ratio edging down slightly to 0.6%.

Other banks in the global top 10 include ANZ, Bank of China (Hong Kong), DBS, Bank of China, Sumitomo Mitsui Financial Group and Bank of Taiwan. DBS delivered strong profitability with a ROA of 1.4% and a CIR of 40%, while Bank of China (Hong Kong) stood out for efficiency, with a CIR of 24.8%. Sumitomo Mitsui Financial Group and Bank of Taiwan posted non-interest income ratios above 40%, highlighting robust diversification. In terms of capital and liquidity, Bank of China (Hong Kong) and ANZ maintained CARs above 20%, while Bank of China (Hong Kong) and Sumitomo Mitsui Financial Group reported strong liquidity, including an LCR of 201% and a net stable funding ratio (NSFR) of 142% for Bank of China (Hong Kong).

Global banking performance

Global banking stability backed by profitability, assets, capital and liquidity

The top 1,000 banks recorded a weighted average ROA of 0.81% in FY2024, unchanged from 0.81% in FY2023, reflecting broadly stable global profitability. ROA declined marginally in Europe and Asia Pacific, while other regions saw modest improvements. Central Asia and Africa recorded the strongest ROA, Latin America and the Caribbean and the Middle East achieved mid-range levels, and Europe and Asia Pacific lagged behind.

The global average net interest margin (NIM) contracted from 2% to 1.8% driven by competitive pressures and rising funding costs. Margin compression was observed across most regions, underscoring persistent challenges in balancing profitability and funding costs. Latin America and the Caribbean, Central Asia and Africa maintained the widest margins, while Asia Pacific and Europe recorded the narrowest.

Operational efficiency improved slightly, with the average CIR down from 49.5% in FY2023 to 48.9%, despite rising technology and regulatory expenses. Banks in Central Asia and the Middle East achieved the lowest CIRs, supported by lean cost structures and solid income generation. Asia Pacific and Africa recorded moderate efficiency, whereas Latin America and the Caribbean saw high operating costs. CIRs remain the highest in North America and Europe, shaped by competitive markets and elevated structural costs.

Income diversification advanced gradually, with non-interest income rising from 34.2% to 35.6% of total operating income. Mature markets showed stronger diversification through fee-based income, while emerging markets — particularly Asia Pacific, the Middle East and Central Asia — remained lending-dependent, with non-interest income ratios below 30%.

Asset quality remained broadly resilient, with the global gross NPL ratio improving slightly to 1.63% from 1.66%. Risks, however, remained concentrated in emerging markets. Africa reported the highest NPL levels globally, which increased further in FY2024, highlighting persistent credit vulnerabilities. Latin America, the Caribbean and Central Asia saw some improvement, but NPLs remained elevated, underscoring the trade-off between strong margins and heightened credit risks.